Local Tax Potential Measurement Must Consider Data Availability

JAKARTA, DDTCNews - The approach used to measure local tax potential must be determined with due consideration of data availability.

Senior Manager of DDTC Fiscal Research & Advisory (FRA), Denny Vissaro, stressed that measuring potential using a complex approach must be supported by comprehensive data. Where data is limited, measurement of local tax potential should be conducted using a simpler approach.

"Ultimately, it is better to have a simple method with complete data than to devise a complex method where the data actually has many gaps," he said at a webinar hosted by the Directorate General of Fiscal Balance (DJPK) entitled "Data-Based Local Tax Targets: Progressive and Measurable Local Tax Planning Strategies", on Wednesday (15/7/2026).

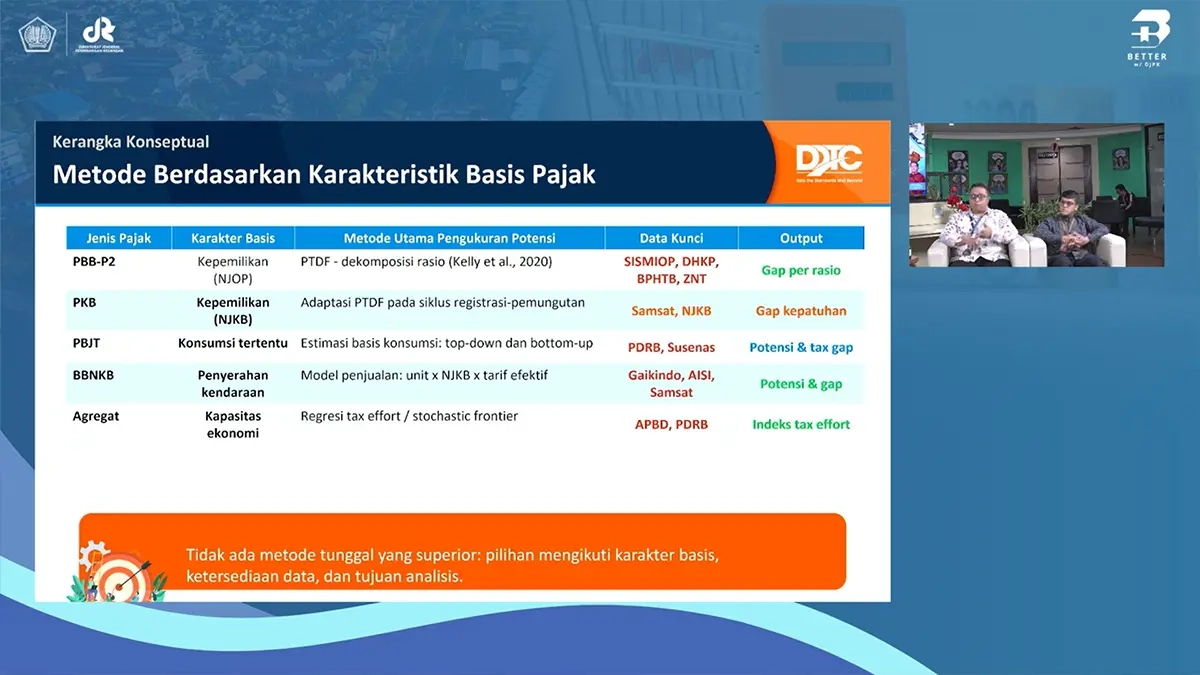

In general, there are at least 2 approaches that can be used to measure local tax potential, namely micro and macro. The micro approach enables local governments to measure potential precisely based on data on taxable objects, transaction data and other detailed data.

Meanwhile, the macro approach enables local governments to quickly estimate local tax potential based on aggregate socio-economic indicators.

According to Denny, the micro approach can indeed provide a more comprehensive overview of the potential of a particular type of tax and the tax gap for that tax type. However, measuring potential using the micro approach also requires comprehensive data.

"If the micro-level data is still limited, we map out the party holding such data whilst simultaneously applying the macro approach first. Ultimately, the two can complement one another [macro and micro]," said the local taxation expert from DDTC.

The use of both approaches above is also conducted with consideration of the characteristics of the type of tax whose potential is being measured.

For instance, where the type of tax being measured is an asset ownership-based tax, such as land and building tax (L&B Tax) and motor vehicle tax (pajak kendaraan bermotor/PKB in Indonesian), data relating to asset valuation, such as land value zones (zona nilai tanah/ZNT in Indonesian) and the sale value of motor vehicles (nilai jual kendaraan bermotor/NJKB in Indonesian), plays a pivotal role.

Where potential is being measured for consumption-based taxes, such as certain goods and services tax (pajak barang dan jasa tertentu/PBJT in Indonesian) and motor vehicle duty (bea balik nama kendaraan bermotor/BBNKB in Indonesian), macro-level data that can serve as a proxy for transactions, such as sectoral gross regional domestic product (GRDP) and consumption figures, is crucial.

"Each type of local tax has a different approach, and we must adapt based on the availability of existing data," said Denny.

Ultimately, both the macro and micro approaches are complementary in nature, so local governments need to use both approaches to estimate the range of revenue potential from a given type of tax under their authority. (rig)